|

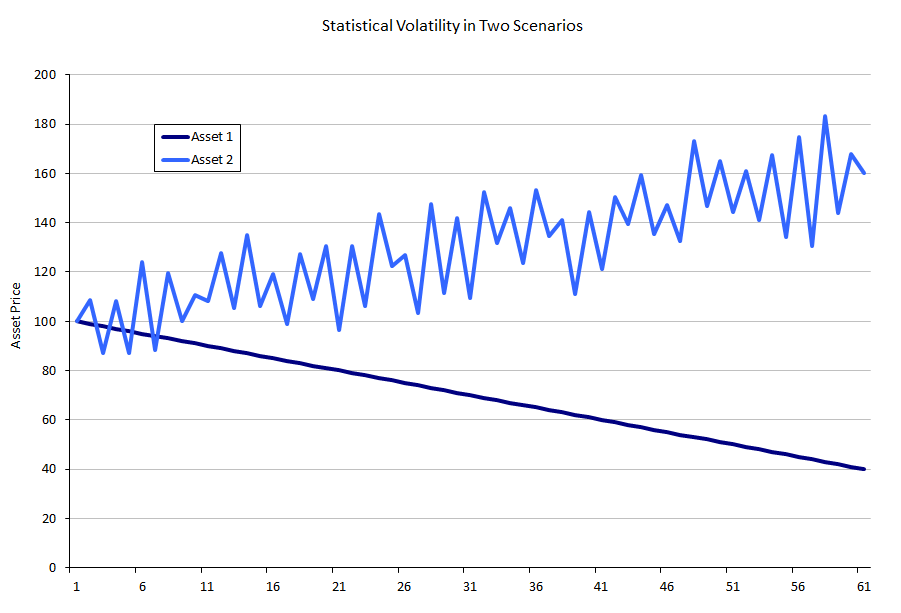

| Asset 1 Volatility = 0.6% Asset 2 Volatility = 350% |

In modern financial theory, volatility is taken to be equivalent to risk. However, I believe it is more helpful to think of volatility as simply “sudden price movement”, since this phrase removes some of the emotional connotations implied by “risk” and is actually more accurate in terms of the underlying mathematics.

Case in point: when I was working as the risk manager for a hedge fund, a fund-of-funds came to interview my portfolio manager and to take statistics of our performance…

Funds-of-funds usually try to figure out which hedge fund would be good to place customer assets by looking at funds’ historical performance and trying to draw conclusions about future performance from that historical data.

About a week after the fund-of-fund analysts had come to talk with us and collect data, a manager at the fund-of-fund called my portfolio manager and said “We like your performance, but the volatility of returns is pretty high, and we are looking for fund with lower risk profiles.” I spent less than five minutes with the performance data and after massaging the data a bit, managed to significantly lower the risk of the fund on a pro-forma basis. I told my portfolio manager, who happily called the fund-of-fund back with a potential solution.

That solution involved pretending that each day our fund had truly exceptional performance, the fund-of-fund client would not receive that day’s performance, but instead be credited with a daily return of 0%. My portfolio manager mentioned that he would be happy to keep that day’s worth of the client’s return. Simply by removing all of the very large upward moves in the fund’s net asset value, we were able to keep a good portion of our returns, but drop our statistical volatility significantly!

The reason this solution worked to reduce “risk” in the mind of the fund-of-fund analyst, was because the fund-of-fund was used to thinking of “large stock price movements” as if they were equivalent to “risk.” This is despite the fact that, if you are long a stock, a large price movement to the upside is not risk, but return!

Does this sound too incredible to believe? I posted an example of this effect using actual trade data for Google (GOOGL) in an Excel file on IOI Tools. Check it out!