One aspect of option pricing that I discuss in The Framework Investing is that very long-tenor options tend to be structurally mispriced. This mispricing allows for an intelligent investor to tilt the risk-reward equation in their favor when investing in LEAPS–especially LEAPS on companies whose statistical volatility is low.

Today, I noticed several news stories about new LEAPS being listed for some large market capitalization stocks. These options will expire in January 2016–giving an investor more than 26 months of economic exposure to the underlying companies.

The LEAPS I saw announced today were on:

The Boeing Company BA

Caterpillar, Inc. CAT

ConocoPhillips COP

At the VALUEx Vail conference hosted by Vitaliy Katsenelson, Kynikos Associates’ founder Jim Chanos presented what he described as his favorite short idea–Caterpillar. His argument deals with the company’s exposure to Chinese infrastructure overinvestment, which he believes to be an issue of epic proportions.

After listening to him speak, I pulled together a quick valuation of CAT and presented an option strategy to gain exposure to CAT’s downside using a put option. Vitaliy posted my CAT presentation on the web, so please take a look at that if you have not already.

|

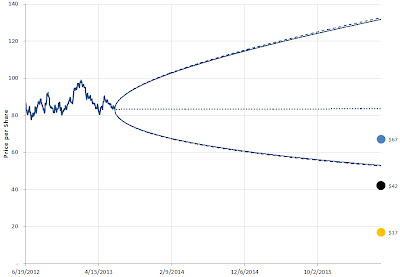

| Caterpillar Valuation Range Source: Company statements, IOI analysis |

As I explain in The Framework Investing, it is better to gain upside exposure through LEAPS than to gain downside exposure, but if Chanos is right about the future direction of iron ore, the January 2015 puts mentioned in that presentation look attractive, and have gotten much cheaper since I originally presented the idea.

I have been meaning to do a more complete valuation of CAT since then, but keep getting sidetracked. This is another of my many back-burner projects that I hope to come back to soon.