In a recent article, I wrote at length about the importance of what Warren Buffett calls “…a sound framework for making decisions…” The framework that I employ is based on an objective, scientific observation of operational measures – revenues, cash-based profits, and investment spending levels – and a clear-eyed view of a company’s growth potential.

To benefit from my framework, I really have to understand how a company creates value for its owners. As such, applying that framework to individual companies has a high up-front “cost” – I have to spend time understanding the dynamics of the business before I have enough information to make an investment decision.

I consider this cost the investment version of the Stanford Marshmallow Test, a person willing to be patient up front will be rewarded amply down the road. A perfect example of how this framework helped me personally is the recent case of pharmacy benefits manager (PBM), Express Scripts (ESRX).

Monday night, a long-time reader, sent a mail through letting me know that Express Scripts had taken a huge price hit in the after-hour trading session after releasing its quarterly earnings. “Is there an investment opportunity here?” he asked.

Figure 1. Source: Interactive Brokers

I looked through the news and within five minutes, sent him back an answer: “Steer clear!” The work I had done up front allowed me to make a sound decision in minutes based on a thorough understanding of the business. I had already made a great deal of money in Express Scripts, and had known that risks were to the downside thanks to the application of a sound investing framework.

Background

I had written extensively about Express Scripts starting in 2015 as it was a large holding of my father’s when he passed away, and I wanted to figure out whether my family should continue to hold it.

Like many investors, my father did not understand what the company did – only that it “has something to do with drugs.” He did know that the company’s stock price had increased dramatically since he first bought it, and that it had split many times. Between the capital gains and the stock splits, the holding in Express Scripts represented a significant proportion of his portfolio’s value – roughly 15% – when he passed away.

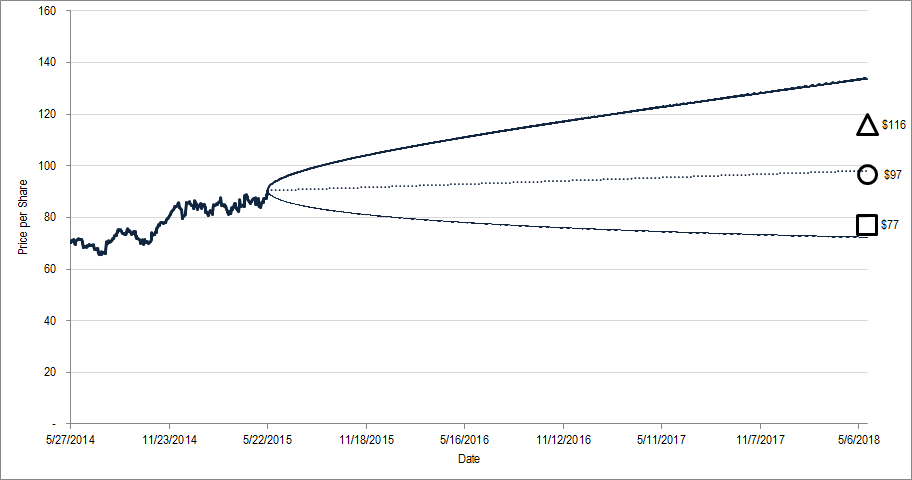

When I originally used my framework to analyze the company’s value, I determined that it was roughly fairly-valued.

Figure 2. Source: YCharts, CBOE, Framework Investing (FWI) Analysis. Geometrical markers show FWI’s best-case (triangle), worst-case (square), and equally-weighted average value (circle). Cone-shaped region indicates option market’s projection of Express Script’s future stock price.

Usually, in this situation, I suggest investing using a passive approach – owning the index is the best idea if an individual company’s shares are fairly-valued. However, my mother was strongly averse to paying capital gains taxes, so I deferred to her wishes and kept the stock in the portfolio.

About a year later, I re-valued the stock. In the interim, the company had announced that its largest client, Anthem (ANTM), had filed suit to recover what it said were excess profits extracted by Express Scripts.

Also, while analyzing the demand environment, it struck me that while the company had built the dominant PBM for the last decade, it seemed to be wrong-footed for the upcoming one. Specifically, it looked to us that PBMs were either shifting to a model that included a retail pharmacy (e.g., CVS Caremark, CVS) or which were incorporated into an insurer (e.g., United Health) and that it seemed Express Scripts was left dangling – especially after Walgreens Boots Alliance (WBA) sealed a PBM agreement with a competitor.

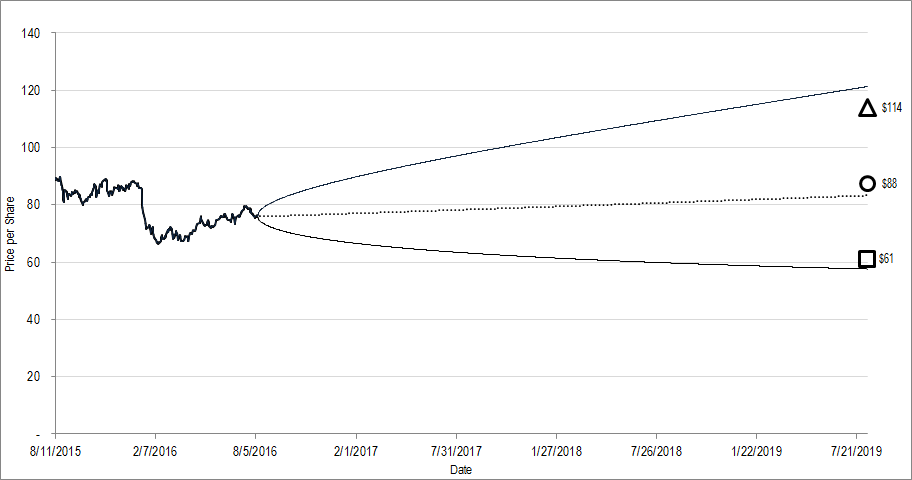

Considering the possibility of Anthem pulling its business from Express Scripts, the shifting competitive environment, and the fact that the PBM business is essentially a zero-sum game, I revised down my revenue growth expectations for the company over the near term, and trimmed my medium-term cash flow growth assumptions. This pulled down my worst-case estimate of the fair value of the firm and, in turn, pulled down the average between the best- and worst-case valuation scenarios by $10 per share.

Figure 3. Source: YCharts, CBOE, Framework Investing (FWI) Analysis. Geometrical markers show FWI’s best-case (triangle), worst-case (square), and equally-weighted average value (circle). Cone-shaped region indicates option market’s projection of Express Script’s future stock price.

While this shift was not large in terms of the average fair value, it did have a big impact on my realization of the risks facing the firm. The possibility of Express Scripts losing its Anthem business was real. My worst-case estimate assumed that Express Scripts would be able to win back other business in subsequent years if it did lose Anthem in 2019.

However, I realized that if the business environment was changing and that the stand-alone PBM model might fall out of favor among clients. I also realized that if Anthem did pull its business and could not replace it, Express Scripts’ cash-based profitability would likely be cut from a half to two-thirds.

In that worst-of-all-cases scenario, I estimated that the new low end of the Express Scripts valuation range would fall to the mid $30 per share range. The balance of risk and reward seemed, to me, to have tipped toward risk. I explained the issue to my mother and closed the entire position over a period of several months.

Monday evening, Express Scripts announced that Anthem would likely not renew its contract after its 2019 expiration. Because I had a sound framework for analyzing the business and the value it created, I understood immediately what this announcement likely meant: a 20% hit to revenues and a good chance for radically lower profitability going forward. I would not be surprised to see Express Scripts’ business suffer from even more defections in the future as clients and potential clients move to a competitor associated with a retail pharmacy or an insurance company.

Relying on a sound investing framework saved my family a great deal of money and allowed me to quickly help someone else make a good decision. That’s the power of a framework in investing.

[embedyt] https://www.youtube.com/watch?v=VaPG4tRztZU[/embedyt]

This article originally appeared on Forbes.com