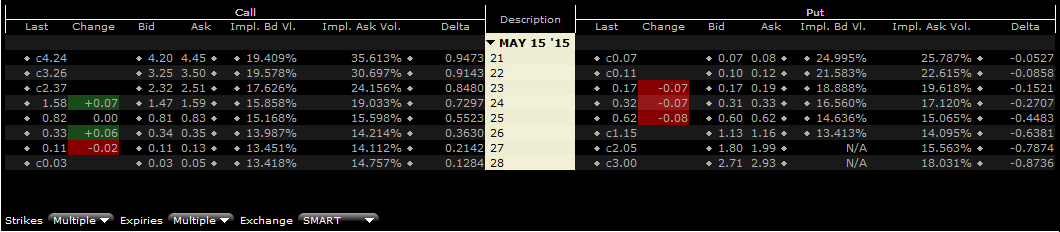

If you were confronted with the following option pricing display, would you know which “Implied Volatility” number most accurately represents the market’s assessment of?the true “Forward Volatility” for this stock?

Figure 1. Option Pricing Screen Excerpt for GE

In the diagram above you see implied volatility values on both the bid side and the ask side of both the put and call option side of the screen. The difference for the implied volatility on the bid and ask side of the 21-strike call option is enormous–over 16 percentage points–and there is a significant “volatility smile” evident in the pricing as well (meaning that implied volatility values are not constant across all strikes).

This is one of the topics we will be covering in the Spring 2015 IOI Boot Camp and the illustration above is from one of the exercise sets for our “Finding Investments” session.

The short answer to the question is that when assessing what the option market is saying about its expectations of forward volatility, it is always best to look to the most heavily-transacted options. Most options are transacted within a 10% band on either side of the present market price of the stock and within tenors expiring in the next three months or so.

For instance, if we look at the above data, my eyes are drawn to the options that are nearest to being “At-the-Money”–the $25 strike price (as discussed in The Framework Investing, ATM options are the ones that have a delta closest to 0.50 on the call side and -0.50 on the put side)

At the $25 strike, the bid and ask implied volatility values are 15.2% / 15.6% on the call side and 14.6% / 15.0% on the put side.

There is a bit more complexity in the details,?but looking at these numbers, my estimate of the?option market’s expectation for forward volatility for this stock is between 15.0% and 15.1%.

This number in turn informs our understanding of the price range the market is expecting for the stock in the future and is the basis for the BSM Cones you see in IOI Tear Sheets and Reports. (This pricing screen happens to be that of General Electric’s option chain and you can see our BSM Cone for GE on the IOI Tear Sheet on GE.)

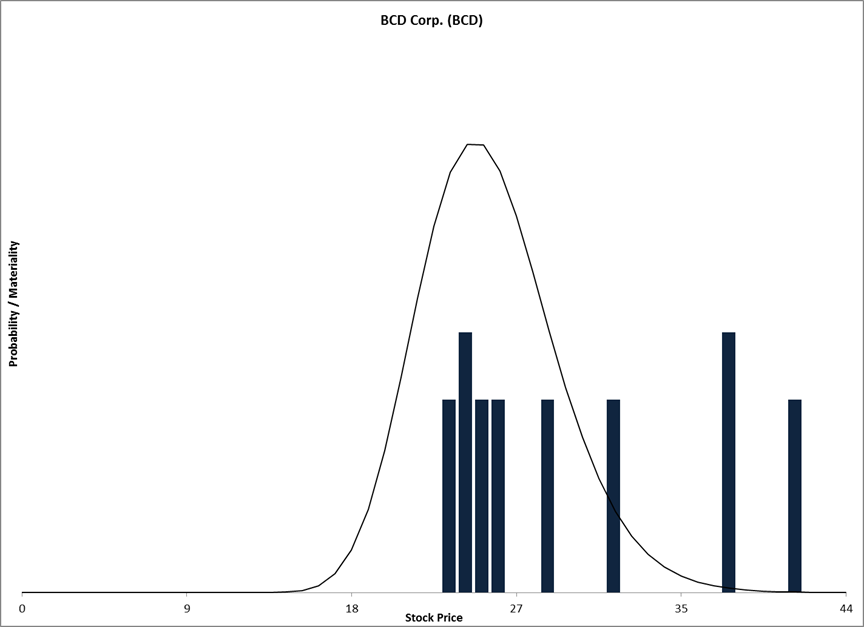

After we understand what the option market is expecting for future prices of a stock, we go on to compare this market expectation to the valuation ranges we create during our?valuation analyses.

The image below is for one of the Boot Camp exercises and not the curve for GE, but you can see the future price range projected by the market represented as a curve. That curve is overlain on a graph of each of our eight valuation scenarios.

Figure 2. Example Valuation Range and BSM Probability Curve for IOI Boot Camp

Comparing the price range expectation of the market with the valuation range estimated by?an intelligent investor is the keystone of intelligent option investing. Becoming skillful at this process?is the prime purpose of the IOI Boot Camps.