Some people collect coins; others collect stamps. I collect examples of companies that most people mistakenly believe operate in a free market. The largest railroad in the U.S., Union Pacific (UNP), is the latest in my collection!

Discounted cash flows are the only sensible way to value a firm if you take the perspective of an owner of the business, but they have one big drawback. Namely, in order to use a discounted cash flow model, you have to select a discount rate. This is a fact that we introduce and discuss in our IOI 100-Series courses and go into greater detail in in the IOI Valuation Master Classes.

As we mention in this post, we like to use a common yardstick for a discount rate depending on the market capitalization of the company. Doing so implicitly makes the assumption that the firm to which the discount rate is being applied competes with other firms of similar size. If we measure UNP according to our common yardstick for a company of its size, UNP looks overvalued.

However, if you assume that because it is a tool of government trade policy (sort of the role that Freddie Mac and Fannie Mae play in housing policy) and reduce the assumed discount rate to 9%, it is fairly valued.

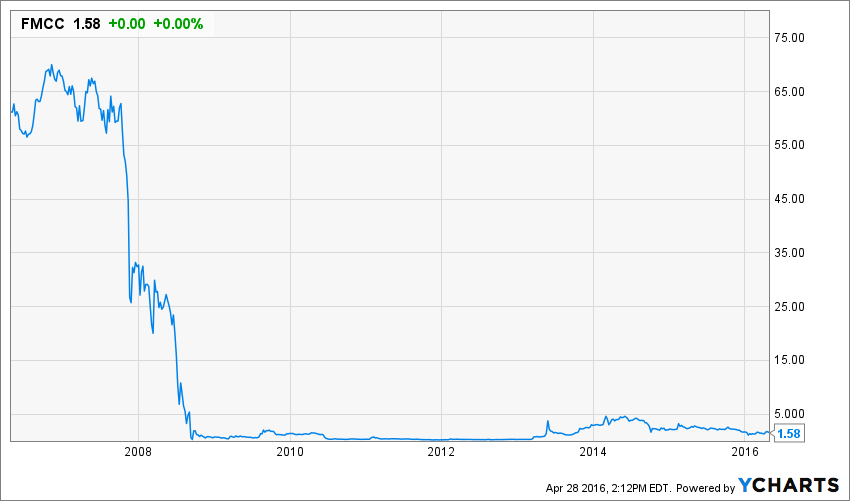

We dislike changing the discount rate for any company – especially since a change in governmental policy could bring the rapid market reassessment of the company’s risk. See if you can guess where this happened in the life of Freddie Mac.

Our most recent IOI Tear Sheet on UNP ![]() discusses what Black Swan option investment might allow you to profit from a re-rating like this.

discusses what Black Swan option investment might allow you to profit from a re-rating like this.