In our IOI Office Hour session last night, we were talking with our members about Under Armour (UA / UAA), when the topic of “inventory write-downs” came up. Beginning investors may have heard this term used by pundits or analysts before, but have been confused about what this term means. This explainer article will shed light on what is essentially a very simple idea. For those who are shaky on the difference between a “Balance Sheet” and an “Income Statement,” work through our Complementary Mini-Course entitled The Language of Business before you read this article.

The first term we should define is “asset.” An asset is:

- Something that can be owned,

- That one must spend resources to acquire, and

- That has the ability to generate net cash inflows in the future.

A piece of equipment is an asset because it meets all those criteria – it’s ownable, you need to spend money to buy it, and you can use the machine to produce something that you can sell in the future.

Figure 1. One example of an asset – a metal-bending machine

By this definition, any product that a company produces with a plan to sell – formally known as “inventory” – is also an asset because it also meets all the criteria above.

Figure 2. Another example of an asset – an Under Armour shoe

Let’s say that a clothing company like Under Armour produces a large amount of inventory. Under Armour cannot produce that inventory without paying suppliers for the input materials – nylon, rubber, cloth, dyes, etc. – and employees or contractors a wage to assemble the items.

Let’s say it costs $917 for all the inputs to produce a certain amount of inventory.

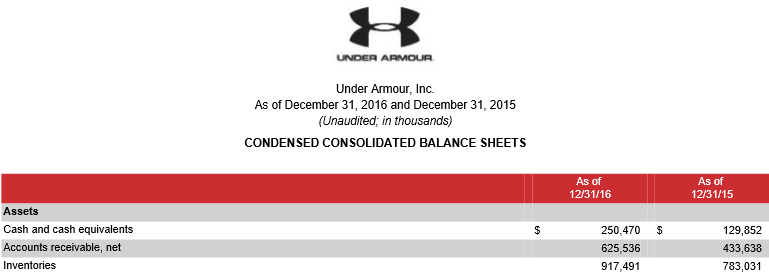

Figure 3. A view of Under Armour’s Balance Sheet. The value of Inventory is $917 million for the company’s 2016 fiscal year.

Under US accounting rules, the value of inventory owned by a company is considered to be “the lower of cost or market.” In other words, the inventory asset in the Under Armour case would be valued at its cost – $917 – unless it was impossible for the company to sell it for that amount. The price for which it can clear its shelves of inventory is called the “market price” of the goods.

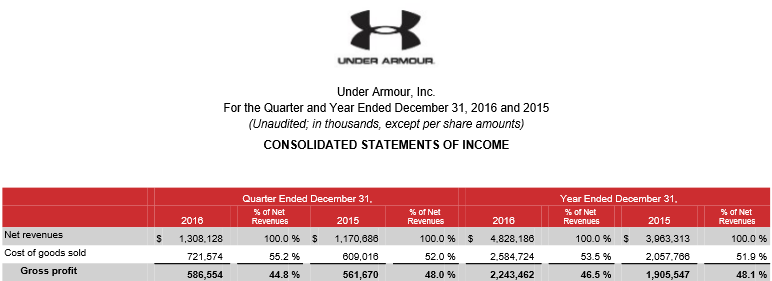

Under Armour is usually able to sell its products for nearly twice what the company paid to produce them (The difference between Revenues and “Costs of goods sold” is known as “Gross Profit”).

Figure 4. You can see the firm spent $721.6 million producing the inventory that it sold for $1.3 billion in the fourth quarter of 2016. Costs of goods sold as a percentage of Net revenues (also known as Gross Margin) was 55.2%. For the full year, the firm spent $2.6 billion on the inventory it sold for $4.8 billion – a gross margin of 53.5%.

This difference between the cost of the inventory and amount of revenue it generates allows the firm a net cash inflow that allows it to pay other expenses (such as advertising, paying salaries to managers, etc.), with any excess available to be distributed to owners or reinvested in the company.

However, sometimes a company will invest in inventory that it cannot sell for the amount of money it took to produce the inventory in the first place.

Figure 5. Would you spend $3 for a set of five of these?

In this case, the firm has to change the value of the inventory it is holding to the “market” price – the price it can get for selling the inventory on the open market.

When the firm does this, it is termed a “write-down” because the value of the inventory is rewritten below the originally announced value. Occasionally, a company will realize that the asset it owns is worthless, in which case it makes a complete a “write-off” of the value of the asset.

A write-down doesn’t only change the value of inventory – the amount of the write-down is treated as a loss on the Income Statement. The accounting term for this is “impairment” – the asset is “impaired” because it is not able to generate enough cash flows as originally expected.

Inventory is not the only asset that can be impaired. If the metal bending machine shown in figure 1 is hit by a meteor, the company will record an impairment equaling its economic value (which, like inventories, is based on the equipment’s cost).

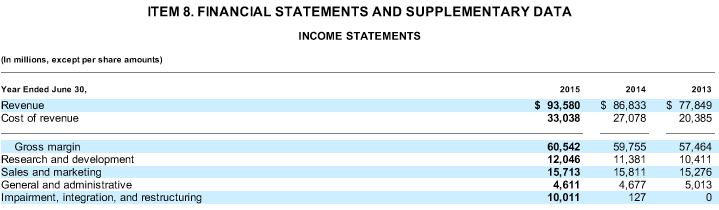

A very notable case of an asset write-down recently was when Microsoft (MSFT) came to grips with the fact that its purchase of mobile phone maker, Nokia, was not going to produce the cash flows it had expected. This is how the company recorded the impairment costs at the time:

Figure 6. Note the large impairment charge in 2015 of over $10 billion. The numbers are shown as positive, but all the line items shown except for “Revenue” and “Gross margin” are costs.

Even though this is recorded as an expense on the Income Statement, it is not something for which the company has to pay out cash. Impairment is today’s acknowledgement that cash spent in the past, was not invested wisely.

In terms of the financial statements, an impairment charge will have a negative effect on Net Income (found on the Income Statement), but there will not be a negative effect on Cash Flow from Operations (found on the Statement of Cash Flows).

A write down is essentially the formal realization that a company’s prior investment – whether that was an investment in materials to produce products that can’t be sold or an investment in an asset like a metal-bending machine or a company – turned out worse than expected and destroyed some part of the owners’ value.

We believe that by looking carefully at Owners’ Cash Profits – IOI’s preferred measure of profitability – an intelligent investor can actually see whether or not a company is destroying the value of its owners before the firm is forced to take a write-down.