One of the most helpful books I have read about investing was George Soros’s trading diary, The Alchemy of Finance. Soros is a macro investor, and his way of approaching investments is very different than mine. However, seeing his comments about what he was thinking about as he invested in a certain sector or region helped me understand how to take a step back and do a meta-analysis of a given investment situation.

Over the past few months, my mother has decided to sell her house and move into a retirement community. She has asked me for help with her investment portfolios, one of which is a retirement account passed on by my father. As I started looking at the portfolio and thinking about what to do in it, I realized there was an opportunity to keep a diary to explain my thought process when approaching the problem. This series of articles is designed to do just that and to give our readers a window into my thinking in the meantime.

The Portfolio

The portfolio is an IRA, so capital gains are not taxable (and capital losses carry no tax shield). Because of my mother’s age and the size of the portfolio (about $1.5 million), she has required minimum distributions (RMD) of just over $100,000 per year, implying that the portfolio should earn at a rate of between 7% and 8% to preserve her principal. (FINRA has a good site with an RMD calculator.)

My father was an avid investor, but was not formally trained, so after his pension converted to a 401(k), approached the problem of managing his money the way a lot of people did: subscribed to newsletters and picked through them for stock tips. He tried a little of this and a little of that while, all the time, developing his own ideas about what worked.

He had an idea that diversification was important and was also subscribed to multiple newsletters, from which he was always getting new ideas. The result was that he ended up with a portfolio characteristic of what we call a “Salad Bar” portfolio.

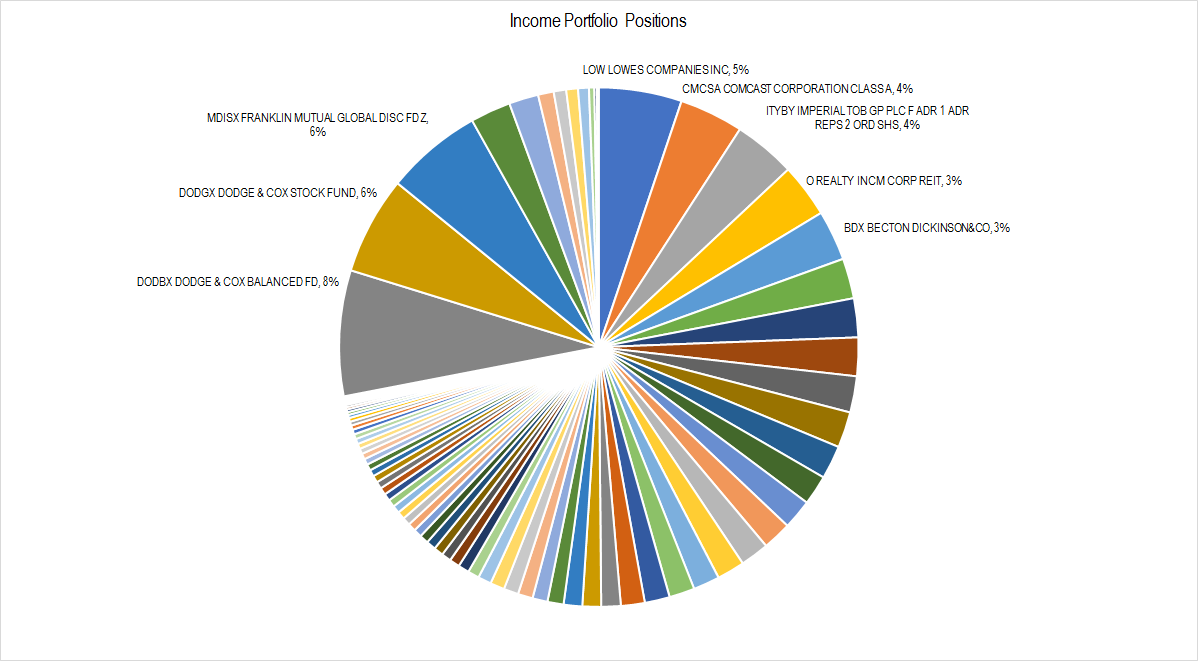

Figure 1.

In total, this portfolio has 86 separate assets, 73 of which are individual stocks, one is cash, and the rest are mutual funds. In the figure above, the stocks are listed in order of allocation size starting at 12 o’clock (LOW). The funds start with the big gray wedge – an 8% allocation to a Dodge and Cox fund. Of the stock positions, 62 of them make up an allocation of 2% of the portfolio or less.

Compared to our goal of drawing an RMD of a little over $100,000 per year on this portfolio, it presently throws off around $40,000 of dividends and interest payments (several of the funds hold a combination of stocks and bonds), implying an average yield of around 2.6%.

We have a lot of work to do. The first step is to define where we are and where we want to go.

Issues

As I see it, there are a few issues that we’ll need to solve with our strategy.

- The yield is too low by about 500 basis points. We want to raise the yield without taking on stupid risks.

- The portfolio is way too complex. The more assets one has in a portfolio the more time and effort it takes just to maintain it. My mother has started sending me emails notifying her of corporate actions and proxy meetings, and I could easily spend hours every week sorting all of these things out.

- It’s difficult to understand the portfolio’s economic sensitivities by just looking at the names. Because there are so many names, it’s hard to know how it will react to different shocks, positive and negative.

- Fund fees eat into the dividend yield. The funds are on the cheap side – 0.5% to 0.6% – but even that is roughly a third of what they are throwing off in dividends.

Strategy

The big focus for me is to simplify. Here is my plan:

- Sell the very small positions that pay poor yields. There are a few stocks with higher yields and small allocations, and I’ll look at those to see if the allocation can be bumped up.

- Look through the larger positions for opportunities. Very few companies are yielding between 7% – 8% these days, but there may be some companies on which I can sell options to boost yield.

- Start looking for preferred shares. Preferred shares are a little ways up the capital structure hierarchy, pay a higher yield, and have less exposure to overall market volatility.

In the end, I’d like to have from 15-20 assets in the portfolio that I understand to about the level of a Five-Minute Valuation, each with an allocation of from 3-5%. This will give me a sense for the fundamental risk factors to which I’m exposed. I’ll also set up a rotating portfolio of maybe 10-20 stocks that I get from screens like the Covered Call Corner, to which I’ll allocate a smaller percentage per security.

I’ll update the community next week with what I’ve done in the interim.