After a tough 2017 in terms of returns, several of Framework’s long-time readers are asking the sensible question “What good is Framework’s methodology?”

Specifically, one member wrote in asking about the bearish positions in Union Pacific and Caterpillar, both of which were very tough positions to love last year, and continue to be difficult positions to love even as I write.

As the analyst responsible for these ideas and the research behind them and as an investor in them, these setbacks have made me ask the same question the member posed to me time and time again, especially during the back half of last year through to the present.

After hours of paroxysms of doubt and deep consideration, I come back to the concept of rational value.

Framework’s approach has – if truth be told – very few “idiosyncratic” elements.* For the most part, the way I analyze companies is the way one is taught to analyze them in graduate schools of business: “The value of an asset is the sum total of cash the asset will generate on behalf of its owners over its economic life.”

Throughout history, this rule has emerged as the intellectual kernel of the field of economic finance simply because it is almost impossible to find counterexamples over the long term.

The catch is the phrase “…over the long term.” A quote attributed variously to John Maynard Keynes and Paul Samuelson — that the market can remain irrational longer than you can remain solvent — is apropos. Over time, the gap between the price of an asset and its value must surely close; however, the interim can create a fair amount of psychological pain.

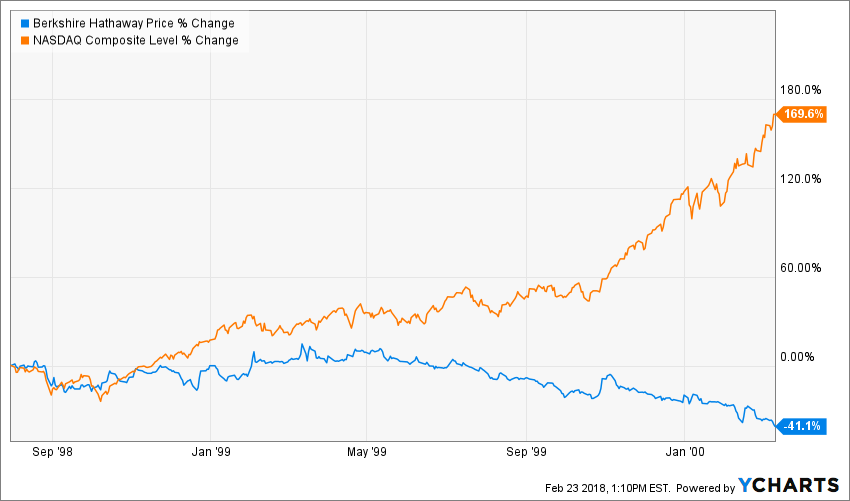

Here is a graphical illustration of psychological pain for one resident of Omaha, Nebraska at the close of the last century.

Figure 1.

Buffett’s Berkshire Hathaway lost 40% of its value simultaneous to the NASDAQ climbing by 170% – a whopping 210 percentage points worth of relative underperformance.

I am not Warren Buffett (and I have the bank statements to prove it), but like Buffett in the late 1990s, I cannot understand why asset prices continue to melt upward while I struggle and fret over bearish positions and an out-of-favor bullish one.

The only thing I know to do is the same thing that I’ve always done — carefully, calmly, and level-headedly look at expectations for companies’ future cash flows, estimate a fair value for those companies using sound methods, and structure investments as appropriate using all the standard tools of modern finance.

Joe has tried to buck me up by pointing out that some of the great value-based investors of our time — Jeremy Grantham, David Einhorn (who is also short Caterpillar), and Seth Klarman — are warning of a crash, turning in terrible performance, and / or have a large proportion of their portfolios in cash. This does not make me feel better. Only being right and being proven right will do anything to improve my mood at this point.

Our mantra at Framework is to provide members all they need — tools, training, and practical examples — to rely on their own judgements when making investment decisions. I’m very proud of the tools and training we offer, even when the examples I have picked have looked more useful as lessons of what not to do so far.

The thing on which we pride ourselves at Framework is the transparency of our valuations and of the research we do. We invite Framework members to pull apart our models, attack our assumptions, and tell us where we are wrong. Doing so — pulling together a model and having us post it on the site — is a good way to start a healthy conversation and is worth a month’s free subscription as well.

Notes:

* The one idiosyncratic element is the selection of a discount rate. I have written a great deal about that, and while I have spoken with many in the business and academia, I have found no one who can offer an argument against my premise in this area.