Overview

The complex, hybrid Oracle investment that I recommended in two different IOI Tear Sheets (late June 2013, and early July 2013) has worked out well thus far. Over the past few months, I have taken profit on several legs as I mentioned I might in my blog posting Oracle, with a nice taste of schadenfreude (December 18, 2013).

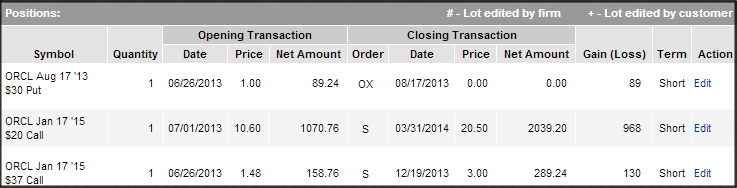

I first took profit on the OTM call on Oracle struck at $37 on December 19, 2013. This OTM call had been paired with a short put struck at $30 and which had expired worthless in August. This strategy–usually called a “Long Diagonal”–subsidizes the purchase of a call with the sale of a put. In this case, I spent a net amount of ($89.24 – $158.76 =) $69.52 on the diagonal. I took profit on the call for $289.24., generating a net profit of $219.72 over 176 days for a period return of 316.0%.

Today, I took profits on the position in the 20-strike options purchase on 7/1/2013. Net gains on the position were $2,039.20 on an investment of $1,070.76 for a 9-month period return of 90.4%.

In total, I spent $1,146.28 to generate a return of $2,328.44 for a return of 103.1%. This compares to a return of 16.4% for the S&P 500 over the 9-month period.

Profit Taking Rationale

37-Strike Call

The rationale for taking profit should always be an assessment of the intrinsic value of the stock. My revised intrinsic value estimate for the stock was $37 per share, with a best-case estimate in the low- to mid-$40s. Given this valuation range, taking profit on the highly levered OTM call position when the stock was trading at $37 / share represents a completely rational decision.

An OTM call is a highly levered instrument. An OTM call paired with a short put in a long diagonal is a very highly levered instrument if and when the short put expires worthless, as it did in my case. By taking profit on the highly levered instruments at a point where its time value is maximized (its 50-delta price), I allowed myself to realize the maximum return possible on the leverage I had purchased. (These references to “50-delta” and “return on leverage” are more specialized and wonkish, but they are not difficult. I cover them more fully in my upcoming book, The Framework Investing, available now for pre-order on Amazon.com).

20-Strike Call

As Oracle’s price continued to rise through the first quarter of this year, it began to inch closer to my best-case valuation price. While the ITM option had much lower leverage than did the OTM one, as the stock price reaches and exceeds one’s intrinsic value estimate of the stock’s value, one should look for opportunities to take profits and reduce exposure to that investment.

It is from this perspective that I decided to close the ITM call position today.

Oracle’s stock price may will climb higher than its present price. Investors sometimes fall into a trap of assessing their investment performance not on their results or on their assessment of the value of a firm, but rather on a hindsight basis. These assessments, which usually start with the phrase “I should have…”, are almost always unhelpful over the long term. Financial markets and companies are complex. If you are very good at valuing companies, you will make money on your investments. However, no matter how good you are at valuing companies, you will never be able to make the absolute maximum of profit on each investment. Chasing such a goal is folly.

The best one can do, in my opinion, is to keep on the lookout for biases in one’s own methodology that causes one to make the same sorts of mistakes over and over again, then to attempt to improve one’s methodology.

Tax Considerations

The account in which I am investing is a tax-free account, so I made my investment and profit-making decisions without respect to tax consequences. Were I making these investments in a taxable account, I would have altered my profit-taking strategy to shift my capital gains more toward long-term ones (which are taxed at a lower rate for U.S. investors and tax payers).

Future Strategy

I continue to hold shares in Oracle and these shares represent roughly 9% of the value of this test portfolio. I am comfortable with this level of exposure, but will likely begin to sell covered calls on these shares if and when the share price increases in the future.

In the mean time, I will continue to look for compelling, intelligent investment opportunities.