It doesn’t matter what the PE Ratio is – Gilead is not necessarily undervalued at present prices. This company is, in our opinion, what many call a “Value Trap.”

This article follows up another article we published in late September just as we were picking up coverage of the company. It is a summary of a detailed report we published to our members, which you can download here.

Gilead is Not a Bargain

Many value investors seem to be enamored with Gilead because it is trading at a “low PE.” However, looking at uncertainties related to opportunities for Gilead’s future growth and considering that its single largest revenue source – its hepatitis c virus (HCV) treatment franchise – is likely to continue to shrink in the near-term, we believe the present price is easily justified by fundamentals. Using a PE ratio or any other multiple to value a firm only obfuscates assumptions for the rate of growth of future cash flows. Gilead’s shares are a perfect case in point why multiples-based valuations are often deeply flawed (See this article for detailed information about why I call multiples analysis one of the Three Great Investing Fantasies).

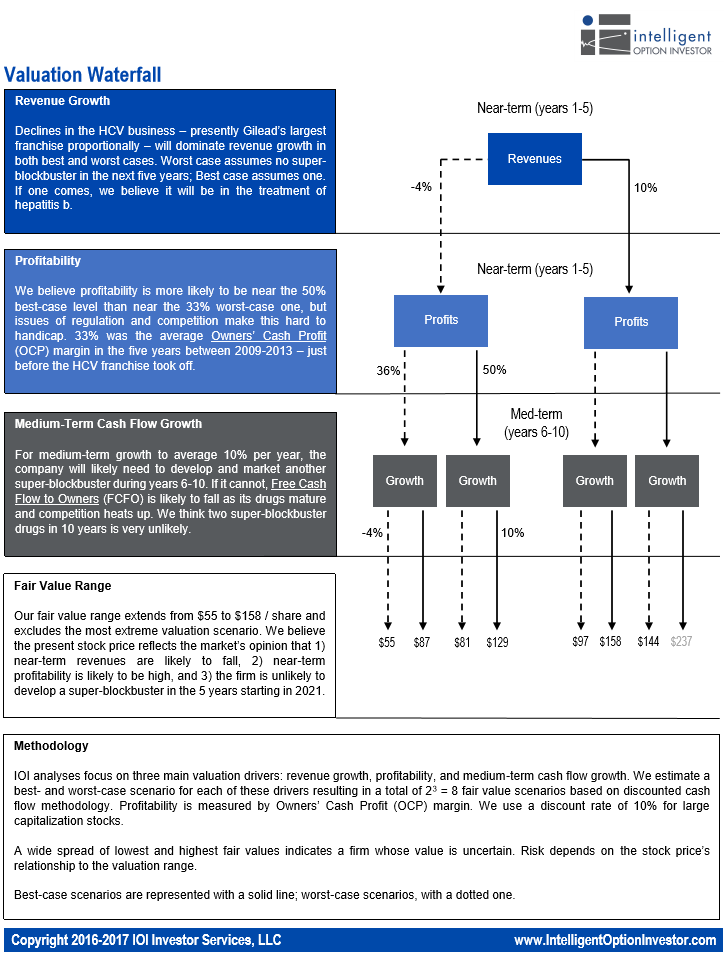

We advocate the use of a valuation range, created by the analysis of likely best- and worst-case scenarios for a handful of key valuation drivers. A summary of the valuation driver assumptions we used to generate the eight valuation scenarios in our range is shown below.

Figure 1. Gilead Valuation Waterfall. Source: IOI Analysis (Download a PDF copy of the Waterfall)

We believe the stock’s present value reflects the market view that near-term revenue growth will be weak, near-term profitability high, and medium-term growth tepid. This last condition suggests that investors are betting against Gilead being able to another blockbuster similar to its HCV franchise in the next 10 years. If the present administration becomes more strident about controlling drug pricing (hereby stunting Gilead’s profits) we believe we could easily see the value gravitating to the $50 – $60 per share range.

Will Lightning Strike Twice? Three Times?

In our opinion, Gilead is, more than anything, a bold and smart biotechnology investor – something like a biotechnology hedge fund.

Gilead’s product portfolio (equivalent to a hedge fund’s investment portfolio) is highly concentrated in two related areas – treatment of HCV and of HIV. As any investor who has studied Bill Ackman or Bill Miller’s career will know, concentration is a double-edged sword. Gilead’s investments throw off a lot more cash than Ackman’s or Miller’s do, and in that respect, are much more robust. However, if Gilead’s future investment projects are not very successful, the company’s value is less than its present price.

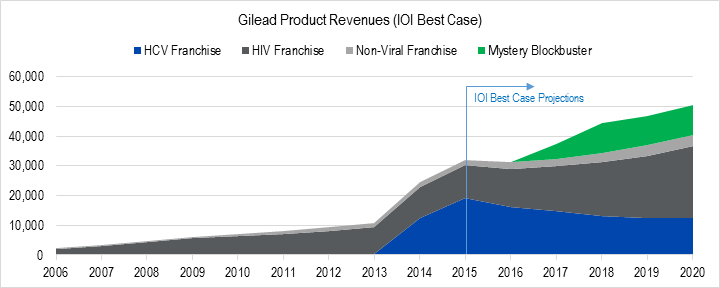

Figure 2. Source: Company Statements, IOI Analysis (Click Here for the full report)

Gilead’s first truly bold investment was the 1999 acquisition of NeXstar, by which it gained access to AmBosome, a treatment for fungal infections that put Gilead on the map. NeXstar’s revenues were three times that of Gilead at the time of the purchase.

The next transformational acquisition was Gilead’s purchase of Pharmasset in 2011, by which it gained access to the drug known as Solvadi, the backbone of its revolutionary hepatitis C virus (HCV) franchise. Pharmasset’s acquisition cost of $11 billion was worth nearly five of the preceding years’ worth of Owners’ Cash Profits (OCP) – IOI’s preferred measure of profitability.

Perhaps because of the enormous success of its HCV franchise, the opinion in some investing circles is that Gilead’s management has some special, proprietary skill in assessing the economic potential of new drugs. We believe that Gilead does have special competence in assessing anti-viral medications, especially treatments of diseases of the liver. We think this suggests its best chance for near-term revenue growth is the extension of its TAF drugs (the newest innovation in its HIV franchise) to the treatment of hepatitis b virus (HBV).

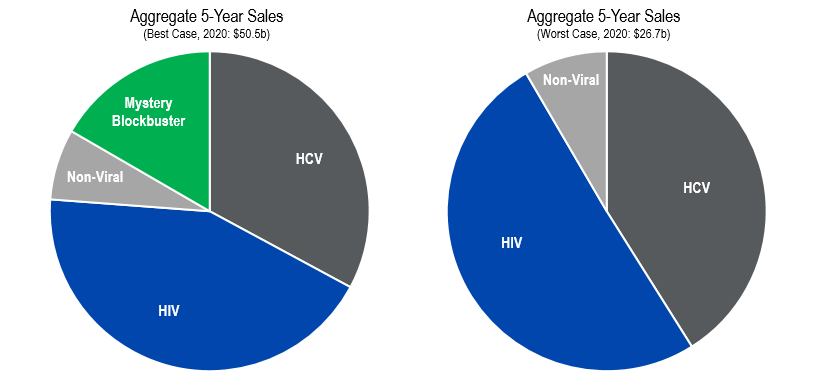

Figure 3. Source: Company Statements, IOI Analysis

If a breakthrough HBV treatment is the “Mystery Blockbuster” shown in figures 2 and 3 (which might be internally developed or acquired), this will be the second time in 10 years that Gilead would have been on the leading edge of a major medical breakthrough. For a normal company, considering the uncertainties surrounding drug development, testing, and approval, the chances of this happening might be near that of lightning striking twice. Still, we think that given Gilead’s experience with the TAF compound and its success in treating HCV make this a possible outcome for the firm.

However, for Gilead’s share price to be boosted significantly, lightning would have to strike yet again during years 6-10 of our forecast period. We believe the chance of this happening is negligible, and have thus excluded the valuation scenario associated with this outcome from our valuation range ($237 / share valuation shown in Figure 1; we left the $158 / share valuation in our range, but think it is very unlikely to occur).

Some in the investment community like to point to Gilead’s NASH pipeline as the source of a possible medium-term blockbuster. We are circumspect for reasons that we discuss in our full report.

This is What a Value Trap Looks Like

Gilead has a strong business, protected by cutting edge research and patents, that throws of an enormous amount of cash (we estimate the firm will generate around $10 billion in Free Cash Flow to Owners in 2016). It is trading for less than 7 times earnings – one of only 18 US-listed companies above $7 billion in market capitalization trading at such a low multiple.

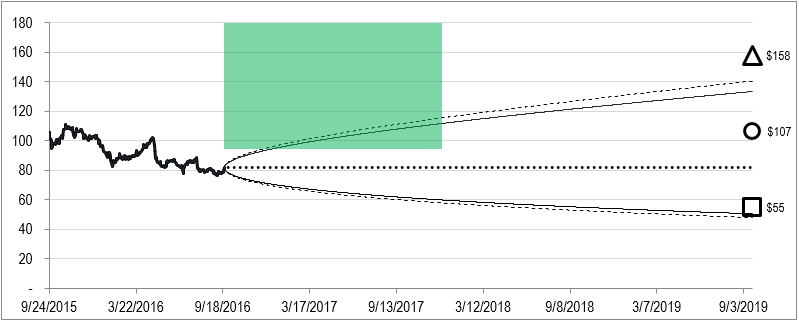

Still, we believe an investor in Gilead has a good chance of – if not losing money – not making money in this in investment for some time. We suggested that if our subscribers wanted to have exposure to the higher valuation scenarios for Gilead, they restrict their investment to speculative Out-of-the-Money call options as shown below.

Figure 4. Source: CBOE, YCharts, IOI Analysis. Geometrical markers show IOI’s best-case (triangle), worst-case (square), and equally-weighted average value (circle). Cone-shaped region indicates option market’s projection of Gilead’s future stock price (dotted line represents ask price projection, solid line, bid price projection). Shaded region represents the purchase of a call option on Gilead’s stock.

Taking the average of our two most extreme valuation scenarios generates an equal-weighted “expected” value of Gilead at $107 / share. If one discards the one other three-lightning-strikes-in-a-decade value of $156 / share, the weighted average drops to around $101 / share.

The $107 per share equal-weighted valuation implies a 50% upside to the stock from today’s close. However, the real possibility of Gilead’s value (which is permanent, unlike “price,” which is transitory) settling at $55 / share – 22% below present levels – means that there is no so-called “margin of safety” to an investment in Gilead at present price levels.

Will Gilead surprise the market with an HBV blockbuster in the next few years? Will the Trump administration crack down on drug pricing and eat into Big Pharma’s profits? Will Gilead make another big, bold acquisition that is its first big failure and turns into an expensive write-down? You may have on opinion on one or all of these questions, but no one can know the answers with even reasonable certainty. In a case like this, investment results rely on chance. As intelligent investors, we would rather be rewarded for our skill and patience.

This article originally appeared on SeekingAlpha and on Forbes.com