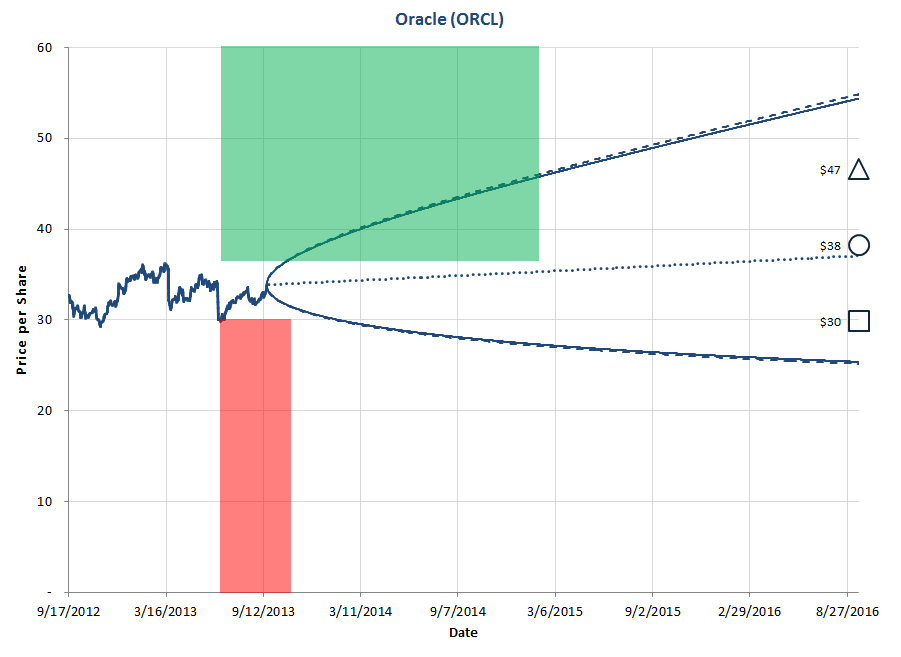

Last Friday, I sold calls struck at $41 and expiring in July of this year on the stock of Oracle ORCL. I received $1.50 / share, making my effective sell price were the shares called ($41 + 1.50 =) $42.50 / share. My sold call options are collateralized perfectly by my long stock position, creating what is known as a covered call. A visual representation of our covered call position in Oracle is as follows:

If the shares are called away, I will realize a profit on the stock portion of my Oracle investment of ($42.50 / $30.00 ? 1 =) 42%.

If the shares are not called away, I will treat the premium received as a sort of special dividend that lowers my average investment cost. In this case, my effective buy price will be ($30.00 – $1.50 =) $28.50 / share.

One of our original positions (a Long Diagonal) in Oracle can be represented as follows:

One of the most misunderstood factors regarding covered calls is thinking that it is a form of profit taking and is thus a bearish strategy. In fact, by exchanging future upside potential for present cash income, we are electing to risk capping future gains while simultaneously accepting full downside exposure.

I do not mind accepting Oracle?s downside exposure and since the stock is trading about 10% above my most recent intrinsic value estimate, I am happy to receive certain cash in exchange for future uncertain returns.

If the model portfolio was more heavily invested, I would likely use some of the proceeds from this covered call to subsidize the purchase of an index put as a hedge for systematic risk.

Option premia are relatively expensive for individual stocks and relatively cheap for indices and other securities representing a basket of stocks (such as a sector ETF). Hedging usually represents a poor economic choice for investors, but there are better and worse ways of doing it; protecting against systematic risk using index options is generally the most efficient method for those who choose to hedge.

IOI