A question came in today from Sheila C., a Registered Investment Advisor who started an IOI Private Coaching course after reading The Framework Investing. She asks a great question about how to structure an investment idea she has been researching.

Her question is one that many people who have used options in their investing eventually run up against: How to select a strike price.

In the auto industry, marketers discovered early on that the more choices they gave customers regarding optional equipment on a car, the worse sales were. Provided?with a lot of choices–a situation?that would seem like a positive–most buyers will react with inaction! This same issue confronts option investors all the time. How can an intelligent investor sort it all out? Here is Sheila and Erik’s exchange.

Sheila C., CFA’s Question

Erik,

I have been doing some “homework? to make sure that I am internalizing what I’m learning. So this has led to a number of questions.

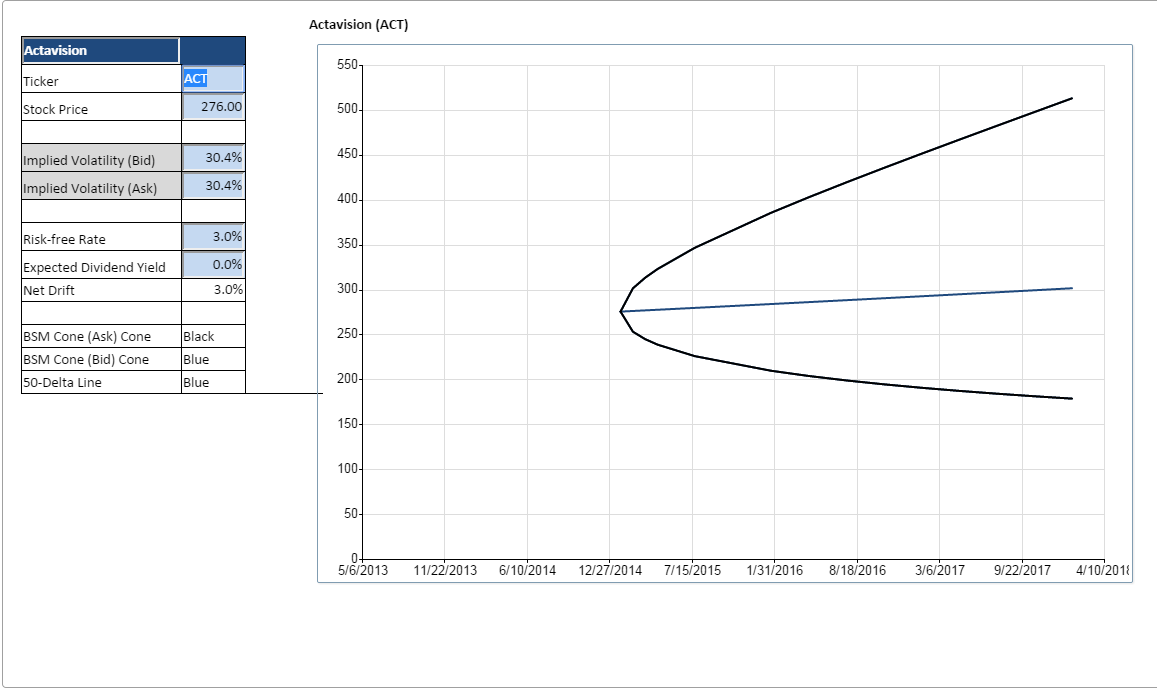

My most recent homework has centered arounds Activis (ACT). I ran the BSM cone using the current month (Feb) ATM options with bid-ask IV. This is the simplified chart since I used the I used just the ask IV.

The current price of ACT is $276. So here is the picture of the cone.

BSM Cone for Actavis (ACT) on IOI Tools

What this tells me is that the most likely price for ACT out to 2018 is $301 with an upside range of $513 and a downside of $179. Morningstar has recently updated their analysis of this company with the acquisition of Allergan (BOTOX). Their current fair value has been increased from $210 to $330 and they have increased the company?s moat from narrow to a stable wide. The company earns a low uncertainty rating with exemplary stewardship.

My questions are these:

- Would you be inclined to view the options as expensive given the implied volatility?

- Just for the sake of our discussion, if you looked at the Jan-17 $250 diagonal [N.B. Erik’s book uses the term “diagonal” to mean a strategy in which an investor simultaneously sells a put and buys a call (a “long diagonal”) or buys a put and sells a call (a “short diagonal”)]. You would be paying around $57 for the call and receiving around $28 for the put. You would be paying for around $32 worth of time and getting premium that covers most of that. Does this make sense if the IV declines over time as the market views this stock as less uncertain?

- Morningstar?s buy price is $264. Assuming that you could get the stock for that price, would you think that buying the stock is preferable to buying the options given that they appear expensive?

Looking forward to talking this afternoon!

Sheila

Erik’s Reply

I’ll just answer briefly here and we can discuss in more detail this afternoon during our session. In short, you’ve not only been doing homework, you’ve been working ahead! You’re asking questions of strategy and structure that we’ll cover in a lot more depth later in the course.

First, on the question about “expensive” options on an implied volatility basis, I actually have written a few things about how to figure out if implied volatility is too high to make an investment or not. Here is a recent one, and here is an older one.

Regarding the Diagonal, what you are describing, selling a put at the same strike price at which you buy a call is actually known as a “synthetic stock” because the risk and return profile is exactly the same as you would get if you bought a stock. The reverse of that (selling a call at the same strike price that you buy a put) would be a synthetic short. I like to think of synthetic long positions in a stock as “renting” a stock, because your exposure only lasts until expiry. You can think about the?net amount of premium you are spending as the “financing cost” for renting the stock until expiration. This might seem a bit confusing, so let’s chat again this afternoon.

Regarding Morningstar’s five-star price, I’m not looking at the option pricing on ACT as I’m writing, but there is probably a way to use options to agree to buy ACT at or below it. Namely, selling a put is essentially promising to buy a stock at a given price at some point in the future and at the put buyer’s discretion.

If you sell a put struck At-The-Money, depending on the expiration you choose, you can generate enough premium income to wind up with an “Effective Buy Price” that is at or below the Morningstar five-star price. I usually look to sell puts with expirations with around three to six months until expiration for a reason that I talk about in the book.

Anyway, these are just brief answers. Looking forward to talking about it in more detail soon.

All the best,

Erik